How to surrender tata aia policy online

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

Tata AIA Life Insurance Co. Ltd will send you updates on your policy, new products & services, insurance solutions or related information. Select here to opt-in.

Thank you for sharing your details. To receive a call from Tata AIA Financial Advisor.

reCAPTCHA is not working.

FOR EXISTING POLICY

Have query on premium, payout or any servicing need?

Dedicated NRI Helpdesk:

Monday - Saturday | 10 am - 7 pm IST

Call charges apply

FOR NEW POLICY

Want to buy a new policy online?

For Indian Residents

Give missed call for a call back:

Monday - Sunday | 8 am - 11 pm IST

Exclusively for NRIs

Data charges may apply

Give missed call for a call back:

Available All Days | 24 x 7

- Tata AIA New Sampoorna Raksha Promise

- Tata AIA Up to 10% Digital Discount Maha Raksha Supreme Select

- Best Seller Param Rakshak Pro

- Trending Param Rakshak Plus

- Param Rakshak (Return of Premium)

- Param Rakshak Elite

- Tata AIA 2% Discount for Women Fortune Guarantee Supreme

- Tata AIA Smart Income Plus

- Tata AIA Fortune Guarantee Plus

- Tata AIA Guaranteed Return Insurance Plan

- Tata AIA Best Seller Pro-Fit

- Tata AIA Smart Health

- Tata AIA Best Seller Fortune Guarantee Pension

- Tata AIA Up to 15% Digital Discount Fortune Guarantee Retirement Ready

- Tata AIA Saral Pension

- Tata AIA New Fortune Guarantee Plus Up to 20% discount on Savings Plan

- Tata AIA New Pro-Fit 10% Discount* on Rider

- Tata AIA Fortune Guarantee Pension Additional annuity of 1%

- Tata AIA New Sampoorna Raksha Promise

- Tata AIA Up to 10% Digital Discount Maha Raksha Supreme Select

- InstaProtect Solution

- Tata AIA Saral Jeevan Bima

- Tata AIA Bharat Suraksha Cover Micro Insurance Plan

- Tata AIA 2% Discount for Women Fortune Guarantee Supreme

- Tata AIA Trending Smart Income Plus

- Tata AIA Fortune Guarantee Plus

- Tata AIA Guaranteed Return Insurance Plan

- Tata AIA Fortune Guarantee

- Tata AIA Smart Value Income Plan

- Tata AIA Diamond Savings Plan

- Tata AIA Gold Income Plan

- Tata AIA Money Back Plus

- Tata AIA Mahalife Gold

- Tata AIA Value Income Plan

- Tata AIA Guaranteed Monthly Income Plan

- Tata AIA POS Smart Income Plus

- Best Seller Param Rakshak Pro

- Param Rakshak IV

- Param Rakshak Elite

- Param Rakshak Plus

- Param Rakshak (Return of Premium)

- Param Rakshak II

- Param Rakshak Prime

- Param Rakshak II 2.0

- Param Rakshak (Return of Premium) 2.0

- Tata AIA Best Seller Fortune Guarantee Pension

- Tata AIA Up to 15% Digital Discount Fortune Guarantee Retirement Ready

- Tata AIA Saral Pension Plan

- Tata AIA Smart Annuity Plan

- Tata AIA Pro-Fit

- Tata AIA Smart Health

- Tata AIA Smart Health Shield Plan

- Tata AIA New Smart SIP

- Tata AIA Best Seller Smart Sampoorna Raksha Pro

- Tata AIA Smart Sampoorna Raksha

- Tata AIA Smart Sampoorna Raksha Plus

- Tata AIA Fortune Maxima

- Tata AIA Wealth Maxima

- Tata AIA Wealth Pro

- Tata AIA Fortune Pro

- Tata AIA i Systematic Insurance Plan

- Tata AIA Smart Sampoorna Raksha Flexi

- Tata AIA New Group Sampoorna Raksha Supreme

- Tata AIA Group Micro Raksha Supreme

- Tata AIA Group Loan Protect

- Tata AIA Group Term Life

- Tata AIA Group Sampoorna Raksha

- Tata AIA Group Employee Benefit Plan

- Tata AIA Traditional Group Corporate Benefit Plan

- Tata AIA Smart Annuity Plan

- Tata AIA Employee Benefit Traditional Plan

- Tata AIA Vitality Protect

- Tata AIA Vitality Health

- Tata AIA Non-Linked Comprehensive Protection Rider

- Tata AIA Non-Linked Comprehensive Health Rider

- Tata AIA Accidental Death and Dismemberment (Long Scale) (ADDL) Rider

- Tata AIA Waiver of Premium Plus (WOPP) Rider

- Tata AIA Benefit Protection Rider

- Tata AIA OPD Care

- Tata AIA Vitality Protect Plus

- Tata AIA Vitality Health Plus

- Tata AIA Waiver of Premium Plus (Linked) Rider

- Tata AIA Waiver of Premium (Linked) Rider

- Tata AIA Linked Comprehensive Protection Rider

- Tata AIA Accidental Death and Dismemberment (Long Scale) (ADDL) Linked Rider

- Tata AIA Linked Comprehensive Health Rider

- Tata AIA Sampoorna Health

- New Capital Guarantee &Income Solution

- Best Seller Capital Guarantee Solution

- Capital Guarantee Advanced Solution

- Secure Insurance Plan

- Most used Term Insurance Calculator

- Most used ULIP Calculator

- Saving Calculator

- Retirement and Pension Calculator

- New Income Tax Calculator

- Most used Child Expense Calculator

- Compound Interest Calculator

- Retirement Calculator

- Human Life Value Calculator

- Home Budget Calculator

- Travel Cost Calculator

- Wedding Budget Calculator

- Startup Valuation Calculator

- Crorepati Calculator

- Dream Car Calculator

- Investment Target Calculator

- Healthcare Cost Calculator

- EMI Calculator

- BMI Calculator

- Cost of Delay Calculator

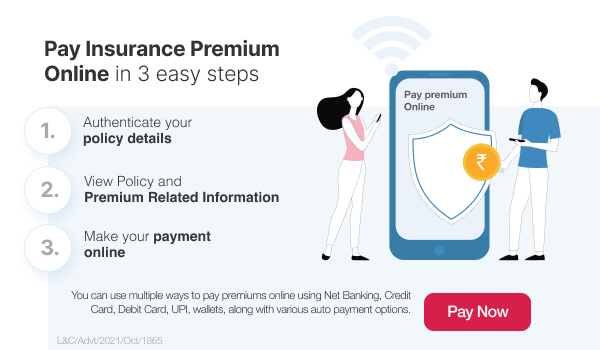

- Online Premium Payment

- Set Standing Instruction

- Cash or Cheque

- Premium Certificate

- Unit Statement

- Account Holder Statement

- Policy Document

- Premium receipt

- Unsolicited Communication

- Service TATs

- Voice of Happy Customers

- Register/Download ABHA

- Unclaimed Funds

- View Fact Sheet

- Bonus and Dividend Performance

- Bonus History

- View NAV

- All Forms

- Bonus History

- Application Form

- Withdrawn Products

- Customer Information Sheet

Term plans

- Tata AIA New Sampoorna Raksha Promise

- Tata AIA up to 10% digital discount Maha Raksha Supreme Select

Wealth plans

- Best Seller Param Rakshak Pro

- Trending Param Rakshak Plus

- Param Rakshak (Return of Premium)

- Param Rakshak Elite

Savings plans

- Tata AIA 2% Discount for Women Fortune Guarantee Supreme

- Tata AIA Smart Income Plus

Retirement plans

- Tata AIA Best Seller Fortune Guarantee Pension

- Tata AIA Up to 15% digital discount Fortune Guarantee Retirement Ready

- Premium Certificate

- Unit Statement

- Account Holder Statement

- Policy Document

- Premium receipt

- Update Mobile Number

- Update PAN

- Update Email Id

- Update NEFT

- Unclaimed fund

- Re-invest

- Electronic Insurance Account

- Switch fund ULIP

- Raise service request

- Login

- Claim Status

- Application Status

- Track your service request

- Our Identity

- Our Products

- Awards and Recognition

- Leadership

- Press Release

- Our Culture

- Corporate Social Responsibility

- HomeBlogsFinancial Planning Surrendering Your ULIP Policy? Here is the Detailed Guide

Need assistance in choosing the right insurance plan? Get a call from our Expert.

Need assistance in choosing the right insurance plan? Get a call from our Expert.

Success

Surrendering Your ULIP Policy? Here is the Detailed Guide

Saving in ULIP insurance must always be a far-headed goal. Any investment made for market-linked returns should be for the longer term. The changes in the investment fund value due to any market volatility situation will get corrected during the longer investment period. Therefore, the fund value will increase and help in wealth creation based on your type of fund option. However, if you choose to surrender your ULIP plan, you will lose out on a certain fund based on the discontinuation charges. Here is a detail about that for your reference.

Before we get started, let us understand what ULIP life insurance means.

What is a ULIP Policy?

A ULIP policy is a comprehensive life insurance plan that provides dual benefits, life cover and market-linked returns. The life cover will provide the death benefit to your family in the event of your unexpected death. And the insurer will provide the market-linked returns at the end of the policy term. Thus, the ULIP policy safeguards your family's financial future while increasing your wealth during the long-term investment.

You can choose the ULIP funds for investment based on your risk appetite, whether equity, debt or hybrid funds. The Net Asset Value(NAV) of the fund will be based on the extent of your investment and the market conditions. There are various charges associated with managing your ULIP investment, such as mortality charges, fund management charges, premium allocation charges, etc. Furthermore, if you have wanted to know how to withdraw the ULIP policy, you can do so after the 5-year lock-in period.

Surrendering ULIP Policy

For any definite reason, if you have decided to surrender your ULIP life insurance investment, you need to understand the financial implications.

Let us consider two scenarios.

Surrendering before ULIP plans lock-in period

- You can surrender the policy before the ULIP lock-in period. The life cover will cease to exist once you surrender the policy. However, the surrender value based on the investment is paid only after the lock-in period of five years.

- The surrender value of the ULIP policy is not based on the fund value as on the surrender date. Instead, it is calculated after deducting certain applicable discontinuation charges.

- The surrender value of the ULIP policy will depend on the individual insurer's policy conditions. It will be based on the ratio of ULIP insurance and investment, mortality charges, fund management charges, etc.

- The investment fund value post deducting the discontinuation charges is transferred to a separate fund referred to as the Discontinued Policy(DP) fund.

- The fund will remain the DP fund until the ULIP reaches the lock-in period.

- A minimum fund management charge not exceeding 0.5% of the fund value applies to the DP fund.

- The DP will earn an interest of 4% per annum until paid for the ULIP after the lock-in period. The interest rate is subject to change based on the IRDAI regulations.

- One other important aspect to note is the taxability* of ULIP on surrender. When you surrender a ULIP policy before the lock-in period, all the tax* deductions you had claimed earlier will be accounted for as income and become applicable for the tax* calculation based on the income tax* slab. Moreover, the surrender value will be subject to the TDS(Tax* Deducted At Source).

- The exit charges for ULIP policies are nil post the five-year lock-in period.

- The charges associated with the ULIP life insurance, such as the mortality charges, policy administration charges, fund management charges, etc., are more during the initial period and further managed by the market value earned. Therefore, it is important to consider ULIP as a long-term investment and stay invested for a longer term, such as 10 to 15 years, to increase the investment fund value.

Tips On ULIP Investment

If you have decided to surrender your ULIP policy due to underperforming investment fund values, you can consider these tips to stay invested.

Reviving Surrendered ULIP policy

Insurance providers offer the option to revive your ULIP policy if you have surrendered it before the lock-in period. The maximum time allowed is within two years of surrendering it. In such cases, the ULIP policy will continue to provide market-linked returns. Also, the deducted discontinuation charges will be added back to your investment fund, and the unpaid premiums will be deducted to start the investment